The IRS released Notice 2021-26 to address taxation of Dependent Care Assistance Programs (“DCAPs”) as it relates to the relief afforded under Section 214 of the Consolidated Appropriations Act, 2021 (“CAA”) and the increased DCAP limit for calendar year 2021 under the American Rescue Plan Act of 2021 (“ARPA”). Briefly, the guidance confirms that:

• With respect to the carryover or extended grace period available under the CAA, if the dependent care benefits would have been excluded from income if used during taxable year 2020 (or 2021, if applicable), these benefits will remain excludible from gross income and are not considered wages of the employee for 2021 and 2022;

• With respect to the increased DCAP limit under ARPA ($10,500), for a non-calendar year plan the increased exclusion amount does not apply to reimbursement of expenses incurred during the portion of the plan year that falls in 2022. In other words, a non-calendar year DCAP generally cannot exclude more than $5,000 in 2022.

Background

As previously reported, Notice 2021-15 provides guidance regarding the implementation of the temporary (and optional) ability under the CAA to allow unused DCAP benefits remaining at the end of a plan year to reimburse dependent care expenses incurred in the next plan year, either due to a carryover or an extended grace period for incurring claims. Briefly, under the CAA, DCAPs may either:

• Carry over any unused DCAP amounts from plan years ending in 2020 to a plan year ending in 2021 (and from a plan year ending in 2021 to a plan year ending in 2022).

• Extend the claims period for plan years ending in 2020 (or 2021) for up to 12 months after the end of the plan year for unused DCAP benefits (extended grace period). In addition, the American Rescue Plan Act of 2021 (“ARPA”) increases the DCAP limit to $10,500 (or $5,250 in the case of a married individual filing separately) for the 2021 calendar year (not the plan year). Unless extended by future legislation, the increased amounts go back to $5,000 (or $2,500) for calendar year 2022.

Treatment of Unused Benefits Made Available in 2021 or 2022

Notice 2021-26:

• Clarifies that DCAP benefits that would have been excluded from income if used during the taxable year ending in 2020 or 2021, as applicable, remain eligible for exclusion from the participant’s gross income and are disregarded for purposes of application of the limits for the subsequent taxable years of the employee when they are carried over from a plan year ending in 2020 or 2021 or permitted to be used pursuant to an extended claims period.

• Explains that in the case of a DCAP in a non-calendar year Section 125 cafeteria plan beginning in 2021 and ending in 2022, the increased exclusion available under ARPA does not apply to reimbursement amounts incurred during the 2022 portion of the plan year. Thus, a reimbursement of more than $5,000 from the DCAP in 2022 may result in a portion of the employee’s contribution becoming taxable upon reimbursement.

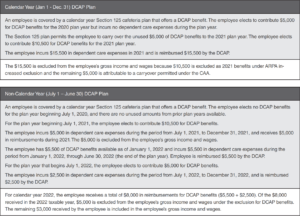

• Provides examples illustrating this guidance, including possible tax consequences of electing $10,500 in DCAP benefits for a plan year that begins in 2021 but ends in 2022 (a non-calendar year plan). The guidance includes helpful examples:

The guidance also includes an example that tackles a non-calendar year plan with the increased DCAP limit plus a CAA carryover.

Employer Action

Employers with non-calendar plans should consider whether to increase the DCAP limit as it relates to calendar year 2021 given the potential tax implications of this design. In addition,be mindful that the increased DCAP limit may cause additional

problems for purposes of nondiscrimination testing. Careful coordination with third-party administrators is important to ensure they understand requirements in Notice 2021-26 and can implement and communicate this information to affected participants. Plan amendments may be required to align contribution and benefit reimbursement maximums with this guidance.

For more information, contact info@benefitsqb.com or schedule a call with us today!